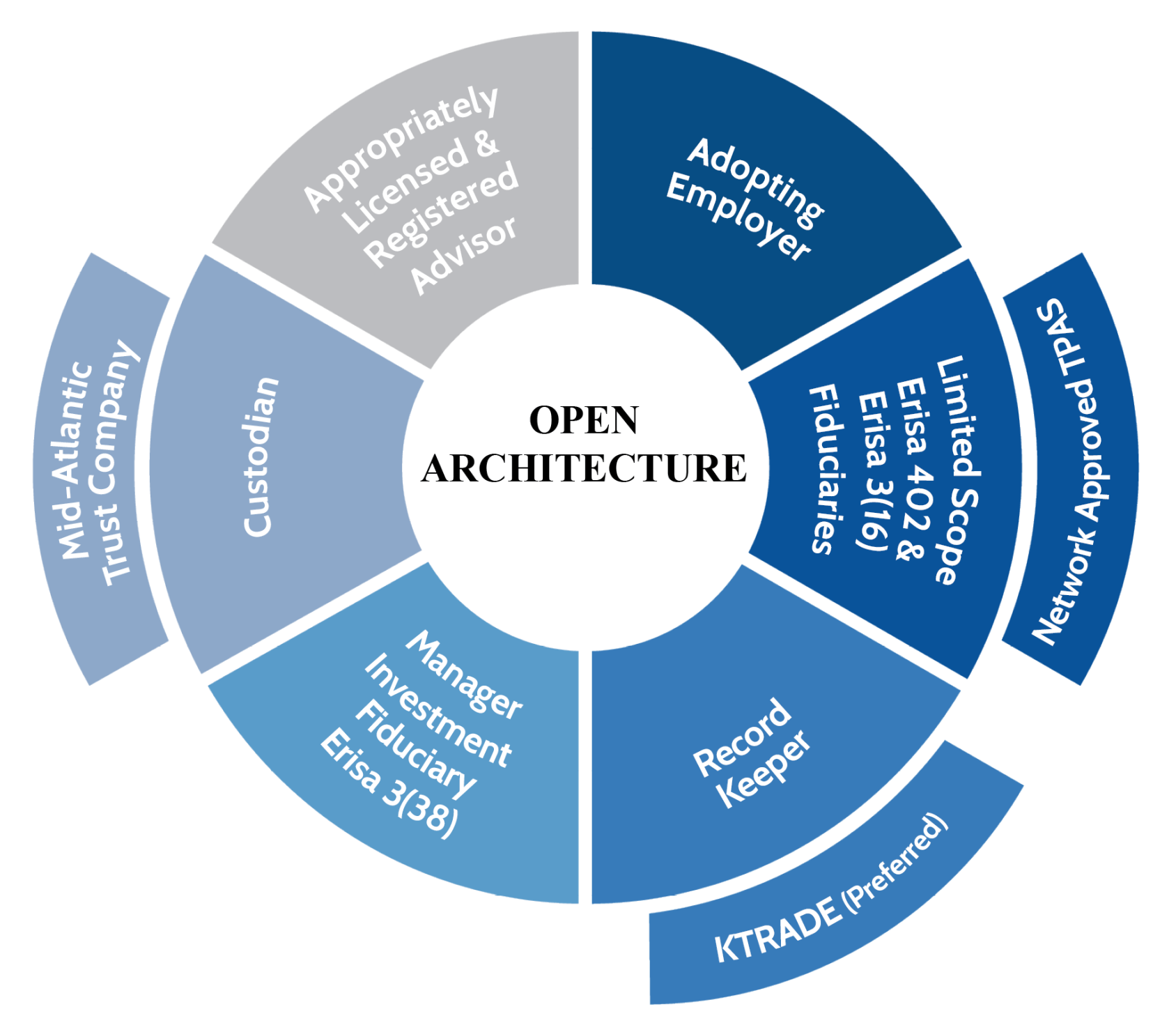

How Does it Work?

For a MEP to work, the following roles need to be filled:

Terry E. DuPont, CRPS, CPhD, CWPP

President & Chief Success Officer

DuPont Wealth Management

Fee-based financial planning and investment advisory services are offered by DuPont Wealth Management a Registered Investment Advisor in the State of Indiana. Insurance products and services are offered through DuPont & Associates, Inc. DuPont Wealth Management and DuPont & Associates, Inc. are affiliated companies. The presence of this web site shall in no way be construed or interpreted as a solicitation to sell or offer to sell investment advisory services to any residents of any State other than the State of Indiana or where otherwise legally permitted.

Licensed Insurance Professional. We are an independent financial services firm helping individuals create retirement strategies using a variety of investment and insurance products to custom suit their needs and objectives. Investing involves risk, including the loss of principal. No Investment strategy can guarantee a profit or protect against loss in a period of declining values. Any references to protection or lifetime income refer to fixed insurance products, never securities or investment products. Insurance and annuity products are backed by the financial strength and claims-paying ability of the issuing insurance company.